Create an XML based language that would describe a set of more complex interface components than those that shipped with the core HTML set. Use this as the foundation of an application framework, something that you could use to create such things as, well, web browsers. Call it the XML User-interface Language (or XUL, because it sounds very much like a demon out of Ghostbusters), and make it freely available.

This was a good concept, but Mozilla had long since lost its edge, Internet Explorer had become the dominant platform for web applications, and anyway, no one was really doing anything with XML on the browser anymore. And then something curious happened. The Mozilla team didn't give up. They kept pushing forward on new technologies, basing them largely on the W3C standards, though occasionally borrowing an idea from Internet Explorer that seemed pretty decent. They also worked to keep up with all of the major platforms (one of the beauties of code abstraction with XML), so that their browsers began to get better, incrementally at first, then faster in the last few years. XUL grew as well, as new components were integrated into the library, and the pieces began to play better with one another.

Last month, Firefox (a light-weight version of Mozilla 1.7) was announced as a release candidate, a near-final version of the application that would let people play with it in depth. As a web browser, it was pretty cool -- fast (though not as fast as it probably will be), easily extensible and skinnable, with a nod to the dominance of Google by the presence of a Google bar and a GMail extension, to RSS feeds by integrated webfeed support, and to XML with estensive XML and RDF functionality built-in (not to mention much more complete CSS support). This combination by itself was enough to make Firefox an intriguing prospect for me when I was looking at building a content-management-system client. I began to port over my code from Internet Explorer, surprised at the relatively minimal pain in doing so, but what I was developing was very much a traditional web page application. However, as I was reviewing the documentation, I kept coming across references to the foundation set used by Firefox ... XUL.

Okay, I have an admission to make. I'm not very good with C++ programming, at least as far as building windowed applications go. Oh, I understand the whole concept of pointers and references, templates make a certain amount of sense to me, and I can generally follow C++ code without a lot of effort, but I found the the whole reference counting, interface querying thing to be entirely too low-level for what I wanted to do - I may as well have been programming in assembler, for the amount of work involved. Perhaps that's why I gravitated to XML in the first place: I liked the notion of being able to abstract the pieces of an application, getting away from the routine and fairly ugly low-level programming that to me seemed should have readily been handleable by a decent compiler. Visual Basic was a big first step in this direction, but it took entirely too long for Microsoft to acknowledge the fact that VB was not a toy (and hence make it easier to access low level operations when need be). Ironically, while the revamping of the underlying interface description language (IDL) into the CLI (Common Language Interface), Microsoft walked away from the simplicity of VB, the thing that in fact made it appealing to beginning (and advanced but harried) programmers in the first place, in order to create VB.NET, which has all of the painful quirks of VB with little of the underlying simplicity.

XUL reminded me a lot of Visual Basic, but in a 2000's XML-ish sort of way. You can create web components with XUL (as I'll show shortly) but XUL ultimately is about application development - creating applications like web browsers, e-mail readers and editors, or even more staid applications such as sales force tools, systems monitors, accounting sofware, and so forth. It has a lot of the features that have become standard in application frameworks, such as layout tools with flexors that resize automatically as the page does, multi-column grid and list elements, toolbars and buttons, fully supported multi-layer menus and menu-popups, and one of the snazziest HTML editors I've ever seen, in or out of an application - and the beauty of all of this is that this capability is sitting within one of the best web browsers on the planet, meaning that once you complete your application, you can make it available as an extension to Firefox itself.

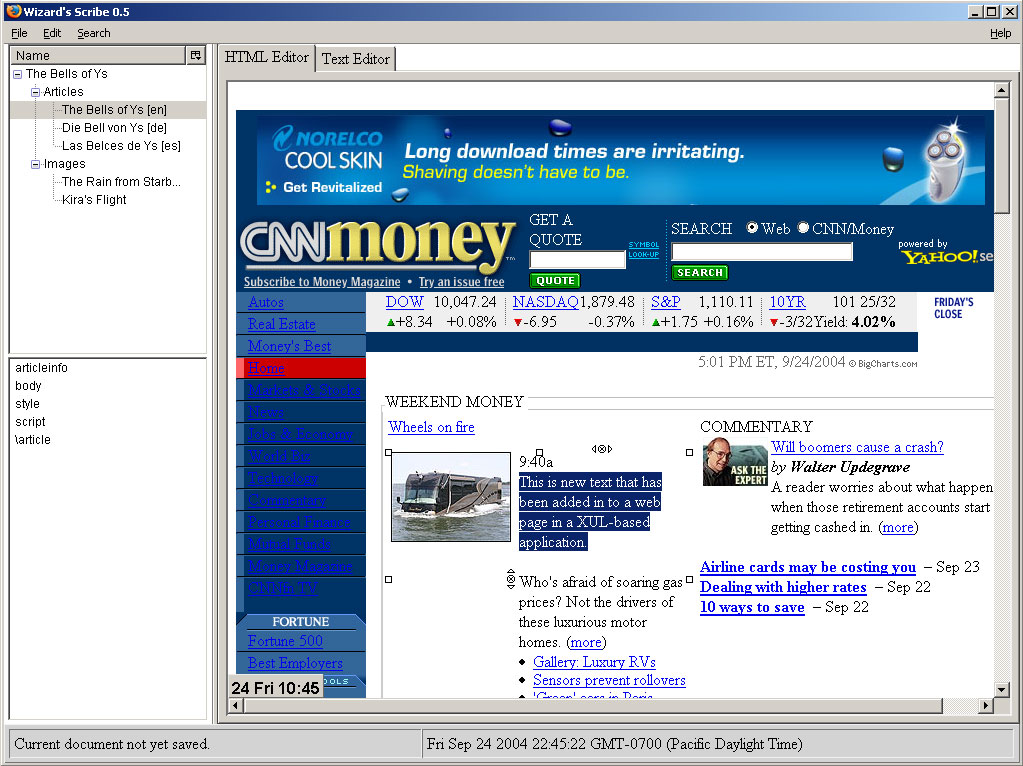

To illustrate the power of this, the following screen shot shows a XUL application I wrote for editing web content:

Screen shot of application built using XUL toolkit.

I didn't write the CNN site, by the way, though I did select the HTML content and drag it into the HTML editor en-mass, something I thought was incredibly cool. It took me about three days to write the app (though I'll admit that I'd done a lot of the groundwork before) and this while I was still learning the basic XUL API. At the moment I'm working at improving it, tying it into the CMS back end that I worked out, but the important thing to consider is that this is a "web application" - no C++, no VB, just a simple XML document and a block of Javascript code.

Actually, more properly, this is an extension. It is downloaded like any of dozens, and likely soon to be hundreds, if not thousands, of other extensions from the Mozilla site (though because of the nature of this application I can't release this version publicly .... working on an open source version, however). It becomes a part of Firefox, something called up from the Tool menu. Because it is part of the browser, this means that it is also within the secure local space, meaning that you can use this toolkit to create sophisticated, multi-platform applications that can be easily downloaded and updated.

This is not all that ideal for a generalized Internet scenario. It is, however, wonderful for the development of intranet (corporate wide) applications. These are the applications that frequently cause some of the biggest headaches for developers, who have to balance between the world of stand-alone applications and the limitations inherent in HTML web-portal applications. If, instead, you can straddle both worlds with an application framework that practically lives on the web, the potential is pretty much endless.

So what does this alien language look like? Here's a sample:

<window

id="findfile-window"

title="Find Files"

orient="horizontal"

xmlns='http://www.mozilla.org/keymaster/gatekeeper/there.is.only.xul'>

<vbox flex="1">

<description>

Enter your search criteria below and select the Find button to begin

the search.

</description>

<spacer style="height: 10px">

<groupbox orient="horizontal">

<caption label="Search Criteria">

<menulist id="searchtype">

<menupopup>

<menuitem label="Name">

<menuitem label="Size">

<menuitem label="Date Modified">

</menupopup>

</menulist>

<spacer style="width: 10px;">

<menulist id="searchmode">

<menupopup>

<menuitem label="Is">

<menuitem label="Is Not">

</menupopup>

</menulist>

<spacer style="width: 10px;">

<textbox id="find-text" flex="1" style="min-width: 15em;">

</groupbox>

<spacer style="height: 10px">

<hbox>

<spacer flex="1">

<button id="find-button" label="Find" default="true">

<button id="cancel-button" label="Cancel">

</hbox>

</vbox>

</window>

This is not the code for the editor, but rather for a dialog box. The root element for XUL is the <window> element, which serves the same purpose as <html> does for HTML. The other elements, including group boxes, menus, buttons and so forth, define specific widgets. For instance, the <button> element defines a button, including it's label, identifier, and default state.

The flex attribute is quite useful. It defines the degree to which the element will attempt to fill up the available space. A flex of 0 indicates that the element will take up the minimal space defined by it's default size, or by it's CSS indicated size if available. On the other hand, a flex of 1 indicates that the element will attempt to expand until other elements push back on it (for instance, a multi-line textbox will attempt to fill the entire window if it's flex is 1, stopped only by other elements. Two or more elements with the same flex will divide the space in half, while two elements of flex 1 and 2 respectively will each take up 1/3 and 2/3 of the available space as appropriate. This simple-seeming innovation can radically cut down on the amount of "resize" code that you have to write.

XUL applications can be run either from a user's local machine (through an RDF based configuration file) or it can be run from the web. The latter case puts some major restrictions of local file access, however, but other than that can work fine. You can embed XUL elements within HTML (for Firefox browsers only, of course) by using XUL's namespace:

xmlns='http://www.mozilla.org/keymaster/gatekeeper/there.is.only.xul'

or you can create XUL applications with XHTML interspersed. Typically, this will require that you modify your server software so that it can legitimately serve up XUL documents recognizable to firefox. In IIS, this would be done by adding the XUL mime-type:

application/vnd.mozilla.xul+xml

to the list of mime-types that IIS is aware of (select the properties pop-up menu item for your server in the IIS control panel, select the Mime-Types button, then add the appropriate associations for .xul as application/vnd.mozilla.xul+xml. With Apache, you add it to the associated mime-types by editing the httpd.conf file.

XUL Resurgent

Interest in XUL has picked up dramatically ever since Firefox came into its own as a separate application, and the combination of ease of use, cross-platform compatibility, intrinsic web awareness and a growing community of developers makes it a technology to watch.

One problem that XUL faces is that the documentation out of the Mozilla site is sketchy at best. However, XULPlanet at http://www.xulplanet.com has several good XUL tutorials and reference documents that are up to date, if not necessarily complete or exhaustive. I would strongly recommend if you're interested in XUL that you check out that treasure trove first.

XUL is, in many ways, analogous to Microsoft's XAML, and with the recent work on the part of the SVG community making its way into the Mozilla effort, I see XUL and XAML effectively going head to head as the first of a new breed of meta-application development languages. XAML is perhaps more exhaustive, but until the Mono effort gets further along, it is not as well represented on non-Microsoft platforms. Additionally, XAML puts a lot more of its emphasis on the use of C# code-behinds, an approach that makes sense for very large enterprise developers but seems like overkill for the average programmer.

XUL may not be your cup of tea, but you owe it to yourself to at least check it out ... as an application framework, it may very well become one of the big technology stories of 2005.

-- Kurt Cagle

121 comments:

For the record, Firefox 1.0 is not "Mozilla 2.0". We are working on a new and exciting "Mozilla 2.0" project with enhanced XUL (especially data-binding capabilities), SVG, optional xforms support, and more.

--Benjamin Smedberg <bsmedberg@covad.net>

Now I'm really confused. I thought Mozilla 2.0 would be a new and improved platform and would take a while. Firefox is based of Mozilla 1.7. I've never heard anything about a testversion of Mozilla 2.0

My bad - Firefox is a lightweight variant off of the Mozilla 1.7 branch. Mozilla 2.0 is considerably more ambitious, as it will include native support for SVG (yeah!!) and probably XForms (yeah!!!!!), and will likely not ship for a year or more. I was a little rushed when I wrote that, and apologize for any confusion.

Hey, you have a great blog here!

I have a build more site traffic web site. It pretty much covers ##Website Promotion## related stuff.

Come and check it out if you get time.

Thought I would try posting to a blog. I have never done this.

Hope I'm doing this right? If I have done anything wrong please let me know.

The only time we have a test before the lesson is in LIFE.

Hey i came here searching for free gay movie porn as i own a site to about free gay movie porn

free gay movie porn

Your site looks good you have good ranking for the terms

free gay movie porn

Well written blog on business hosting site web I have a related blog on business hosting site web

Lots of good sony electronics information here. Also check out sony electronics if you get a chance. I was able to lear a lot.

Market oi millions with blogblastermarketing careermarketing career

Please go to http://ww.blog-masters.net

Imagine Thousands Of Links Back To Your Web Site From Other People's Blogs!

came here cause i thought your site had free black porn movie

u should check out free black porn movie

Good Blog

Please visit

Advanced Business Marketing

and leave a comment.

I have seen a lot about home based business opportunity.

See how a 33 yr old ex-bouncer replaced his income and learned even more about home based business opportunity

Seriously, It only took about nine months. There is a lot of hype out there about home based business opportunity so don't get overwhelmed.

It's real though. A sixty year old industry that does $100 Billion a year in sales. Isn't that worth ten minutes of your time?

Click Here Now

display your RSS feeds on their web sites for content.

For the best in music business software visit online stores for DVD Software Players that offer quality audio playback on the PC.

Sometimes, these gambles pay off, but there are occasions when they fail miserably,

Thanks for offering this great service to learn about sports odds. I have a website about sports odds which makes me very interested in what you have going here. I think I am going to start up my own blog so I can spread the news! Thanks you are offering this great service!

Nice Blog about car part wholesale. I also have a Blog/Website about car part wholesale which is why I enjoyed this blog so much. Keep up the excellent work! Check out my site if you have a moment.

Use our affordable directory ecommerce host web to get your web hosting site seen. Increase your chances of getting quality traffic and increase your revenue through or straight forward affordable directory ecommerce host web

Not much to say besides the fact that coming to Register Better would be a good decision in regards to yahoo domain registration !

Join the 3 Marketeers Club today, its Absolutely FREE!!

I look forward to Your visit!

hey speaking of free things try blingo for free limewirefree, its free to sign up and you can win free prizes! I just won a free movie ticket! Lets win together!

Great Blog you have here!

I'm definitely going to bookmark this one.

Do you know DOT WS (website) will be larger than DOT COM (commercial) ?

Remember 800 phone numbers? Now you have 888 877 etc.

Are you a visionary? I hope you are and decide to get in on something

that will change your life! GDI is where its at.

7 day free trial and no selling

Want a short .WS domain name? Now you can get one and make affiliate $$$$$$$

You get your own website

Check this one out :-)domain registrydomain registry

www.getipodsforfree.com has this cool thing where if you just sign up and do an offer, you can get a free ipod

Increase your Search Engine Rank in Days noy Months!

Hey I have 42 free free cartoon porn mpeg at my blog! You can download them all, no problem, Think of them as porn trailers. Free Videos

You can post a comment to your website at my blog too :) Thanks!

I was looking for soft porn video and came across your blog. I have a Free Videos site that has over 40 sample porn mpegs. I hope you enjoy them.

Feel free to place a comment and a link back to your website on my blog.

So your interested in canada porn news

There is a new Adult Press Release site out there to release adult porn related news!

Its called Porn Biz

Check it out canada porn news

www.TheOnlinePromoters.com has everything a webmaster needs to succeed online

Shop at your favorite stores 24 hours a day. Why go to the mall when you can shop online and avoid the traffic

Your blog is perfect and nice, we are offering premature ejaculation help to learn more visit premature ejaculation help or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

premature ejaculation help http://www.manifestingpower.com/premature-ejaculation.html

Very nice blog you have here. Searching for unique blogs with random words. Carrots, guppy, car part albuquerque, sword fish, running shoes. Anyway, take care and good blogging.

Your blog is perfect and nice, we are offering to learn more visit or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

http://www.manifestingpower.com/premature-ejaculation.html

thanks for the info

Your blog is perfect and nice, we are offering premature ejaculation treatment to learn more visit premature ejaculation treatment or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

premature ejaculation treatment http://www.manifestingpower.com/premature-ejaculation.html

Your blog is creative Keep up the great work. Maybe you could stop by my site sometime here: penis enlargement directly

This is a excellent blog. Keep it going. I found you while searching for penis enlargement service. I have a site on penis enlargement service located here, penis enlargement service Maybe you can stop by sometime.

Some of the most useful information I came across today. When searching for potencx penis enlargement , I had come across your site. Always a pleasure to see other blogs related to my site potencx penis enlargement Keep up the great work.

Your blog is perfect and nice, we are offering sexual problem to learn more visit sexual problem or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

sexual problem http://www.manifestingpower.com/premature-ejaculation.html

Your blog is perfect and nice, we are offering premature ejaculation to learn more visit premature ejaculation or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

premature ejaculation http://www.manifestingpower.com/premature-ejaculation.html

Never thought I'd find your site looking for cheap computers. Strange. Good stuff. Think I'll try another term. Nice blog.

I like it! I like it! Keep up the good blogging!

web site design

Your blog is perfect and nice, we are offering pre ejaculation to learn more visit pre ejaculation or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

pre ejaculation http://www.manifestingpower.com/premature-ejaculation.html

Hi there...nice blog. When I was out blog surfing looking for detailed info on as seen on tv products I found your page. Your site is not an exact match but it did catch my interest. Should you ever need information on as seen on tv products then drop by the site above and check it out.

www.TheOnlinePromoters.com has everything a webmaster needs to succeed online

Good stuff! I enjoyed your blog.

professional web site development

Your blog is perfect and nice, we are offering male ejaculation to learn more visit male ejaculation or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

male ejaculation http://www.manifestingpower.com/premature-ejaculation.html

I appreciate your blog. Well done, even though it's not mine! Just kidding! Off to find web site development and promotion or something like that. Take care.

Hi Kurt, I was just blog surfing and found you! Wow, I really like this one.

It’s such a pleasure to read your post …. Interesting! I was over at another site

looking at Outsourcing

and they didn't go into as much detail as you, but nonetheless interesting.

Your blog is perfect and nice, we are offering sex problem to learn more visit sex problem or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

sex problem http://www.manifestingpower.com/premature-ejaculation.html

Great stuff.

free palm software

Your blog is perfect and nice, we are offering stop premature ejaculation to learn more visit stop premature ejaculation or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

stop premature ejaculation http://www.manifestingpower.com/premature-ejaculation.html

Hi there! While out blog surfing today for specific info on as seen on tv ads, I ended up on your page. Your site shows that I ended up a little off base, but I am certainly glad I stopped by. I will bookmark your site for a future visit, and should you ever need it, there is plenty of information on this site about as seen on tv ads.

The ultimate internet marketing website is www.TheOnlinePromoters.com

Have you seen any information on bullet as seen on tv? I just have not had the best results when blog surfing today. Anywho back to my endless search for bullet as seen on tv.

It's time to take charge of your future and independence by having your own business!

thanks for the info

like the blog gay

Congratulations Friend for your excellent blog on who is domain search!Keep up the good work!

If you have a moment, please visit my site:

who is domain search

I send you my warm regards and wish you continued success.

Have a nice day! :-)

Your blog is perfect and nice, we are offering premature ejaculation cure to learn more visit premature ejaculation cure or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

premature ejaculation cure http://www.manifestingpower.com/premature-ejaculation.html

You ever have an annoying dog that barks next door like a mad crazy dog from a Carpenter book and you all of sudden find yourself at the computer on the internet and completely absorbed? And for those few solumn, focused and unearthly moments, you could not hear that damn dog barking in the background until you somehow get detached from the computer. But when I got back on my computer, I have no clue how I ended back searching for Halifax mortgage uk when my original subject was completely different than that. Hmmmm, it must be that I was drawn to this specific site. Funny how things works.

Halifax mortgage uk

I wonder if anyone will ever truly believe that they can find out what started life on this planet and the origin of it. I mean, it is almost as abstract as opening your browser and venturing to find out something as random as Mortgage providers in the uk and not even knowing a thing about it. And then actually learning about it, the root of what started it. You know?

Mortgage providers in the uk

Some days I feel like rambling here on my blog, but other days it is about giving my readers just what they want. And I had a special request the other day about something. Now I cannot even remember it. So being the curious guy I am, one day, I went out to the engines to find only the best sites about ##leyword## a visitor to my blog had requested. And wouldn't you know it, the site came up in the first search. Always a nice shocker. Hey, maybe I'm reallly getting good at this.

How to host your own web site

This is a great opportunity. Just push a button 4 times per day and make $1,000's per month within one year.

So where do we go from here, my girlfriend says. And you know what I told her? I said to her, I do not know about you, but I am going to search for something about Design host hosting site web and for God sakes, I am going to find it. Then maybe later we can resume this supposed important topic. Sounds like I am real determined, huh? Well, I found it, that site, the one on that thing I was searching days and days before. Yeah, it was perfect. Go peak at it even if the topic sparks your interest at the slightest.

Design host hosting site web

Your blog is perfect and nice, we are offering male ejaculation to learn more visit male ejaculation or Who ya gonna call? XUL!! http://www.manifestingpower.com/premature-ejaculation.html

male ejaculation http://www.manifestingpower.com/premature-ejaculation.html

Not ever again! Never again will I go anywhere else for stuff on Online mortgage lender uk than this one site I just found. Woah! I am blown away by the wealth of info and other resources on this site. If you have personally been struggling to find out more about where you can access that kind of info, you will listen to me and soon discover how easy it is to find out more about it.

Online mortgage lender uk

I always found car racing funny, especially the Indy 500. I mean, how tired are these guys

riding around in a circle with each other for like 500 miles or so? I mean, I understand the

skill of racing others, but there's nothing like a true change of scenery. Mortgage brokers in uk

From a single home PC to a multi million dollar enterprise. you can't afford to lose youe valuable data.

Link to my site:data free pro recovery software

Hi Kurt, If you would like to send your ad to the best opportunity seekers please click here Safelist.

http://www.submitterbizz.com

Safelist

Acne or pimples are caused by hormonal changes, wrong food habits and improper skin care. Some Acne remedies are based on herbs and natural ingredients that treat your Acne like magic and help improve the skin disorders.

Link to this site: acne treatment and prevention

http://www.acne-faq.info/

Hi,

Bought a new car and i am looking for consumer electronics sales .

Can aynone here give me info ?

I tried to search for it on blogger but cannot find anything.

I did find a bunch of blogs but not really focused on my search.

Thks

Cassandre

Just blogging for a while, my site is also about web hosting frontpage, so just saying what's up.

Charles

Hi, Just browsing around for ideas for my site. (While we're at the same topic), I'm just getting started if you want to visit:

web hosting plan

Charles

Just blogging for a while, my site is also about web design hosting services, so just saying what's up.

Charles

I just read your blog, � very nice.

I made myself a blog, I have a movies download site. It pretty much covers movies download related stuff. Check it out if you have the time.

Hello,

Hi! I�m writing to ask you if I could duplicate the information/idea you published on your site, on to my website. I think it�s a fantastic idea! I look forward to hearing from you.

Thanks,

make money extra

Hello,I found the ideas on your site to be original and very well thought out. I will continue to visit your site regularly. Thanksmoney fast make online

Hi,

We would be interested to know if there is a way we can get notified of new posts on this blog. We are usually busy but find your blog nice and need to get notified of something new:)

Regards,

online fast make money

Hello ##NAME##, with all the information on work from home I became very overwhelmed. Anyway, I was online doing a specific search for the most current information on work from home and somehow I ended up on your site. ##NAME## to be frank, ##TITLE## wasn't not the exact match to what I was looking for, but boy am I glad I'm here. You've certainly managed to grab me attention and peak my interest. I must say this is a great blog and I'm most certainly happy that I stopped by eventhough it wasn't the work from home related information I was looking for. Thanks. Keep up the good work.

Hello ##NAME##, with all the information on work from home I became very overwhelmed. Anyway, I was online doing a specific search for the most current information on work from home and somehow I ended up on your site. ##NAME## to be frank, ##TITLE## wasn't not the exact match to what I was looking for, but boy am I glad I'm here. You've certainly managed to grab me attention and peak my interest. I must say this is a great blog and I'm most certainly happy that I stopped by eventhough it wasn't the work from home related information I was looking for. Thanks. Keep up the good work.

You blog sure gets quite a few comments. I'm going to read thru your posts and see why you are generating so much interest.

Hi there...nice blog. When I was out blog surfing looking for detailed info on mineral make up as seen on tv I found your page. Your site is not an exact match but it did catch my interest. Should you ever need information on mineral make up as seen on tv then drop by the site above and check it out.

Good comments. But, I do not agree with most of them. People sure have a lot of time on their hands. Ms.

Hello. I was blog surfing and your blog caught my eye. I have a cool site that may interest you. If your not interested, then I am sorry for bothering you. Go to free affiliate programs.

Hi Blogger:)

Very entertaining and useful blog. Yours attracted me so much that I shall come over here more often.

Regards,

make money at home online

Hi Blogger,

I don't usually read too much, however this was an exeption to the rule! I even re-read certain things on your blog

cause I found them very interesting.

Regards,

make money at home online

I was searching blogspots on Google and found yours. Nice read keep up the good work.

From http://www.surveyearn.biz/PaidSurveys/Work_at_home.html which is about work from home

Good Blog Site with a lot of intersting and not so interesting comments I would say!

If you have a moment please feel free to visit my site http://www.surveyearn.biz/PaidSurveys/Work_at_home.html

work from home

First Class!

- http://www.surveyearn.biz/PaidSurveys/Work_at_home.html - mom work from home

Such interesting and informative comments on your site.

If you require some small business web design info come to my site at http://www.small-business-web-design.ssr.be

web design company Interior Design - Do You Love Decorating Your Own House? Get Paid!

Are You Ready To Start Your Career In The Interior Design Industry?

A Designer creates, organizes and designs commercial and residential properties. A designer works with the interior of a particular space and various internal spaces.

How To Break Into The Design Industry is a thoroughly researched report on how to take your interest and turn it into a full fledged career. It takes you from the beginning - helping you figure out if this is really for you - all the way to finding clientele for your new business. Interior Design web design company

web ecommerce design - keep up the good work. I had a nice read on this site

web design Interior Design - Do You Love Decorating Your Own House? Get Paid!

Are You Ready To Start Your Career In The Interior Design Industry?

A Designer creates, organizes and designs commercial and residential properties. A designer works with the interior of a particular space and various internal spaces.

How To Break Into The Design Industry is a thoroughly researched report on how to take your interest and turn it into a full fledged career. It takes you from the beginning - helping you figure out if this is really for you - all the way to finding clientele for your new business. Interior Design web design

Great blogsite you have here! Interesting information, come and visit mine sometime web design company

Hello, we have just finished creating this free questions and answers forum for members of The Country Club Biz. Please check it out at Country Club Biz Forum

I find your Blog interesting - some thoughtful comments abound!

You are welcome to come visit my site http://www.spyware-beware.com/Spyware/Spyware_Detection.html which is about spyware blockers

I enjoyed reading through your blog and experiencing your perspective on things.

Regards,

home work help

WHAT IS THISSSSSSSSSS

If You are looking for more info on book and am glad to be on your site. If you want to find out more about......book then go visit http://ibooks4u.com......You wont be disapointed..Thanks For Visiting

Doing the Google search found your blogsite. Some content here is very thought provoking. Not sure i agree with all but hey this is a democratic world - on the whole!!

All the best and respect, from Dave - http://proof.sitesell.com/web-sales22.html which is about web site design

Nice blog. Loved all the free online adult movie. Keep up the good work and I shall return.

This blog looks good and works well - good info and content. a firm fan at small business

Hi Kurt, today I’m surfing for a good blog

experience on remove spyware and I found your great site.

Well this post wasn’t exactly what I was looking for

it did receive my attention and interest. I see now

why I found your resourceful web-site when I was

searching for remove spyware related information and I am

glad I found your site even though its not an exact

find. Let me contribute to this site by leaving you

with my favorite quote from Nicholas Negroponte! -

"Computing is not about computers any more. It is

about living." --- Nicholas Negroponte ---

Hey there Kurt, I was looking for an educational blog experience on internet business income opportunity and I found your blog-site. Who ya gonna call? XUL!! isn’t exactly what I was searching for but it did get my and interest. Now I know why I found your excellent blog-site when I was looking for internet business income opportunity related information and I’m glad I did even though its not an exact find. Great Informative Post, thanks for the read and educational experience.

Hi Fellow! I was just searching blogs,and I found yours! I like it!

If you have a moment, please visit my bad credit loans site.

Good luck!

Hi, just wondering if anyone knows any other great affiliate programs. I'm currently using Dating-Solutions.com (http://www.dating-solutions.com) as i find there product second to none! But im looking at spreading my wings and finding other affiliate program directory, so if you know of any affiliate program directory. Please respond to my message. I recomend anyone who's in the adult/dating industry to check out http://www.dating-solutions.com as there just great! - Let me know how you get on!!! Rachel x

Great blog....now...ADVICE TIME!! - If you need more expired web site domain with traffic then congratulations I've come to the right place, try expired web site domain with traffic - this is the best place online to get massive volumes of internet traffic back to your blog for blog publicity purposes. Within a week I had trippled my volume of traffic - Signup is free and before you know it you will flying up the Google search egine - guaranteed!! - Signup is free you have nothing to lose. Best of luck with it and continued success with your blog!!

affair seeking woman

Hi

Sorry to intrude but I saw your blog, noticed you have anonymous posting enabled and thought you might be interested in this great search engine optimization tool for your blog and website (if you have one) that a techi mate recommended to me. Apparently it's all the rage in the IT arena.

I am involved in affiliate best program and I've found the best way of promoting my blogs and websites is The amazing link referral program. Don't worry it is absolutely free to join and you can generate visitors to your site by visiting others. It is really quick and easy to set up and the traffic you generate will help your website increase in google ranking. Give it a go now!!

I have generated amazing traffic from this program - increasing my affiliate sales and cannot recommend this enough. Believe me, if you have tried all the other programs on the market that you have had to pay for then you realise this one is the best - and it's free!!!

Best of luck with the blog!! I hope you get as much out of this program as I have ;-)

.

Hi matey

I'm sure it was this blog I was reading a while back where someone was looking for an SEO tool for driving more traffic and get more hits for their website.

Anyway, I was speaking to a techi guy at work who gets to know all the latest stuff and he uses the free Link Referral Program.

His website on denver search engine optimization amongst other stuff has seen traffic explode since he started using the Link Referral Program - consequently his affiliate sales commissions and business sales went through the roof PLUS his website increased in google ranking which was an added bonus!!

If anyone else has any good ideas for driving more traffic to blogs/websites then please share with your online business blog buddies. Ta ;-)

.

myspace tweaks

.

RE: issue in economics today

Thanks for recommending the free Link Referral Program for search engine optimization (seo) - I've signed up and am considering upgrading to the affiliate program - looks like a winner to me!!

.

A pal of mine had a website featuring seo copywriting and he was desparate for more website traffic. He scoured the internet and tried all the pay-for software programs including Trafficseeker, Addweb, IBP and many, many, more. All they succeeded in doing was crippling his site's page ranking and cosequently he plunged down the google search engine ranking. He then discovered a new way of getting genuine visiting traffic back to his webitse.

The system has been such a success that he has upgraded his account and now refers others up to the program.

If you are looking for free website promotion, free traffic, free marketing, free advertising then look no further Linkreferral is here!!

Hey, you have a great blog here! I'm definitely going to bookmark you!

I have a vending business opportunity site/blog. It pretty much covers ##KEYWORD## related stuff.

Come and check it out if you get time :-)

Free Porn Videos, with no popups or redirects, blisteringly fast porn downloads for teen, hardcore, milf, mom, asian, lesbian, amateur, webcam girls,

2000% INTERNET PROFITS

.

Hi matey

I'm sure it was this blog I was reading a while back where someone was looking for an SEO tool for driving more traffic and get more hits for their website.

Anyway, I was speaking to a techi guy at work who gets to know all the latest stuff and he uses the free Link Referral Program at http://marketingexperts.wordpress.com.

His website on mlm home based business amongst other stuff has seen traffic explode since he started using the Link Referral Program - consequently his affiliate sales commissions and business sales went through the roof PLUS his website increased in google ranking which was an added bonus!!

If anyone else has any good ideas for driving more traffic to blogs/websites then please share with your online business blog buddies. Ta ;-)

home based business

home based business opportunity

internet home based business

home based web business

best home based business

home based business idea

home internet based business opportunity

start home based business

best home based business opportunity

online home based business

income opportunity home based business

legitimate home based business

home based business lead

mlm home based business

starting a home based business

top home based business

christian home based business

home based small business

home based internet marketing business

free home based business

work at home based business opportunity

computer home based business

home based mlm business opportunity

make money home based business

home based business work

home based travel business

easy home based business

serious home based business opportunity

small home based business opportunity

online home based business opportunity

home based business for woman

business opportunity home based work from

work from home based business

new home based business opportunity

start a home based business on the internet

based business business home opportunity

legitimate home based business opportunity

home based sales business

home based jewelry business

best rated home based business

home based franchise opportunity business

successful home based business

home based business opportunity idea

profitable home based business

internet home based business idea

home based business work at home

best home based business idea

home based business opportunity work at home

free home based internet business

home based business tax deduction

top home based business opportunity

home based computer business opportunity

unique home based business opportunity

home based affiliate business

home based business opportunity uk

income opportunity home based business idea

based business home incredible opportunity

based best business home small

starting home based internet business

christian home based business opportunity

home based business merchant account

best home based internet business

based business home network opportunity

home based business marketing

based business home idea latest

home based business review

home based business directory

based business career home opportunity

work at home based internet business

based business home job opportunity

home based business trade secret

best home based business

home based business magazine

home based computer business idea

home based business startup idea

home based business for sale

home based business cash opportunity

home based business web site

most successful home based business

.

Dear administrator:

Some of our comments above may include links that are no longer valid or that do not have a nofollow value. They might very well lead you today to a third party. Therefore,

I ask you, if you would be so kind, to please delete or disregard those

comments.

Many thanks and best wishes,

Iza, Roberto Iza

Muy Señores Míos:

Algunos de nuestros comentarios incluyen vínculos rotos que bien pudieran llevar hoy a una tercera persona. Por tanto, le rogamos, por favor, que los deseche o desestime.

Gracias y recuerdos

Iza, Roberto Iza

If your credit card uses different rates for purchases, transfers, and cash advances, realize that the card issuer may pay the lower interest rate balance first. Consequently, if you carry a balance, your high-rate cash advance may not be "paid" until all lower-rate balances are paid in full.

Fixed-Rate credit cards are not fixed forever. Rates can be changed at any time, as long as the card issuer provides 15 days advance notice of the change in terms. Fees may also increase. These "Change in Terms" notices are usually included with your monthly statement.

Your interest rate may dramatically increase if you make late payments. For example, some issuers will raise your interest rate to the maximum after one or two late payments. Consequently, your 12% credit card could quickly turn into a 25% credit card.

Your credit card issuer may also raise your interest rate after conducting a routine credit report review. If your overall credit history has deteriorated, the issuer may raise your interest rate, even though you've never made a late payment on the card in question.

The 25 day grace period only applies when you pay-off your entire balance due each month. If you only pay the minimum payment, interest is immediately accrued from the moment you charge something to your credit card. Some companies are also shortening the grace period to 20 days, and some cards have no grace periods.

Ignore offers to reduce or skip payments. These options are frequently offered over the holidays. When you skip a payment, the loan continues to accrue interest; therefore, these offers simply increase the overall interest and finance charges that the creditor collects. On a similar note, beware of offers of no payment/no interest for a period of time. Furniture stores, jewelry stores, and electronics stores frequently offer these programs. For example, no payment/no interest for 12 months!! This can be a good offer, but once again, read the fine print. Make sure you know the details of the program. Generally, you need to pay off the entire balance before the end of the "free" period to receive the benefit. Otherwise, you will probably have to pay interest on the entire balance from the date of your purchase

Debt1consolidation.com entails taking out one loan to pay off many others. This is often done to secure a lower interest rate, secure a fixed interest rate or for the convenience of servicing only one loan.

Debt1consolidation.com can simply be from a number of unsecured loans into another unsecured loan, but more often it involves a secured loan against an asset that serves as collateral, most commonly a house. In this case, a mortgage is secured against the house. The collateralization of the loan allows a lower interest rate than without it, because by collateralizing, the asset owner agrees to allow the forced sale (foreclosure) of the asset to pay back the loan. The risk to the lender is reduced so the interest rate offered is lower.

Sometimes, debt consolidation companies can discount the amount of the loan. When the debtor is in danger of bankruptcy, the debt consolidator will buy the loan at a discount. A prudent debtor can shop around for consolidators who will pass along some of the savings. Consolidation can affect the ability of the debtor to discharge debts in bankruptcy, so the decision to consolidate must be weighed carefully.

Debt consolidation is often advisable in theory when someone is paying credit card debt. Credit cards can carry a much larger interest rate than even an unsecured loan from a bank. Debtors with property such as a home or car may get a lower rate through a secured loan using their property as collateral. Then the total interest and the total cash flow paid towards the debt is lower allowing the debt to be paid off sooner, incurring less interest. In practice, many people are in credit card debt because they spend more than their income. If that habit continues, the consolidation will not benefit them much because they will simply increase their credit card balances again.

Because of the theoretical advantage that debt consolidation offers a consumer that has high interest debt balances, companies can take advantage of that benefit of refinancing to charge very high fees in the debt consolidation loan. Sometimes these fees are near the state maximum for mortgage fees. In addition, some unscrupulous companies will knowingly wait until a client has backed themselves into a corner and must refinance in order to consolidate and pay off bills that they are behind on the payments. If the client does not refinance they may lose their house, so they are willing to pay any allowable fee to complete the debt consolidation. In some cases the situation is that the client does not have enough time to shop for another lender with lower fees and may not even be fully aware of them. This practice is known as predatory lending Certainly many, if not most, debt consolidation transactions do not involve predatory lending.

Credit card debt is an example of unsecured consumer debt, accessed through plastic credit cards.

Debt results when a client of a credit card company purchases an item or service through the card system. Debt accumulates and increases via interest and penalties when the consumer does not pay the company for the money he or she has spent.

The results of not paying this debt on time are that the company will charge a late payment penalty (generally in the US from $10 to $40) and report the late payment to credit rating agencies. Being late on a payment is sometimes referred to as being in "default". The late payment penalty itself increases the amount of debt the consumer has.

When a consumer has been late on a payment, it is possible that other creditors, even creditors the consumer was not late in paying, may increase the interest rates the consumer is paying. This practice is called universal default.

If the customer is carrying an amount of debt that is so high that it is over their credit limit, then they might be charged an over-the-limit fee of up to $39 until their balance is paid down to below their credit limit. This, too, may add to the consumer's debt.

Sometimes the late fees, over-the-limit fees, high annual percentage rates (APRs), and universal default overcome consumers who frequently do not pay off their debt, and the customer declares bankruptcy. If a customer files for bankruptcy, the credit card companies are required to forgive all or much of the debt, unless such discharge of debt is successfully challenged by one or more creditors, or blocked by a bankruptcy judge on legal grounds irrespective of creditors' challenges.

Because forgiveness of debt reduces likelihood of profit and continued survival, the companies are generally willing to offer another deal to the consumers in danger of bankruptcy. This deal consists of reduced APRs, removal of past late fees and penalty charges, and reaging the accounts so that the credit agencies see them as late accounts.A credit card is a system of payment named after the small plastic card issued to users of the system. A credit card is different from a debit card in that it does not remove money from the user's account after every transaction. In the case of credit cards, the issuer lends money to the consumer (or the user). It is also different from a charge card (though this name is sometimes used by the public to describe credit cards), which requires the balance to be paid in full each month. In contrast, a credit card allows the consumer to 'revolve' their balance, at the cost of having interest charged. Most credit cards are the same shape and size, as specified by the standard.

A user is issued credit after an account has been approved by the credit provider, and is given a credit card, with which the user will be able to make purchases from merchants accepting that credit card up to a pre-established credit limit. Often a general bank issues the credit, but sometimes a captive bank created to issue a particular brand of credit card, such as or Banks issues the credit.

When a purchase is made, the credit card user agrees to pay the card issuer. The cardholder indicates their consent to pay, by signing a receipt with a record of the card details and indicating the amount to be paid or by entering a Personal identification number (PIN). Also, many merchants now accept verbal authorizations via telephone and electronic authorization using the Internet, known as a Card not present (CNP) transaction.

Electronic verification systems allow merchants to verify that the card is valid and the credit card customer has sufficient credit to cover the purchase in a few seconds, allowing the verification to happen at time of purchase. The verification is performed using a credit card payment terminal or Point of Sale (POS) system with a communications link to the merchant's acquiring bank. Data from the card is obtained from a magnetic stripe or chip on the card; the latter system is in the United Kingdom commonly known as Chip an PIN, but is more technically an EMV card.

Other variations of verification systems are used by eCommerce merchants to determine if the user's account is valid and able to accept the charge. These will typically involve the cardholder providing additional information, such as the security code printed on the back of the card, or the address of the cardholder.

Each month, the credit card user is sent a statement indicating the purchases undertaken with the card, any outstanding fees, and the total amount owed. After receiving the statement, the cardholder may dispute any charges that he or she thinks are incorrect (see Fair Credit Billing Act for details of the US regulations). Otherwise, the cardholder must pay a defined minimum proportion of the bill by a due date, or may choose to pay a higher amount up to the entire amount owed. The credit provider charges interest on the amount owed (typically at a much higher rate than most other forms of debt). Some financial institutions can arrange for automatic payments to be deducted from the user's bank accounts.

Credit card issuers usually waive interest charges if the balance is paid in full each month, but typically will charge full interest on the entire outstanding balance from the date of each purchase if the total balance is not paid.

For example, if a user had a $1,000 outstanding balance and pays it in full, there would be no interest charged. If, however, even $1.00 of the total balance remained unpaid, interest would be charged on the $1 from the date of purchase until the payment is received. The precise manner in which interest is charged is usually detailed in a cardholder agreement which may be summarized on the back of the monthly statement. The general calculation formula most financial institutions use to determine the amount of interest to be charged is APR/100 x ADB/365 x number of days revolved. Take the Annual percentage rate (APR) and divide by 100 then multiply to the amount of the average daily balance divided by 365 and then take this total and multiply by the total number of days the amount revolved before payment was made on the account. Financial institutions refer to interest charged back to the original time of the transaction and up to the time a payment was made, if not in full, as RRFC or residual retail finance charge. Thus after an amount has revolved and a payment has been made that the user of the card will still receive interest charges on their statement after paying the next statement in full (in fact the statement may only have a charge for interest that collected up until the date the full balance was paid...i.e. when the balance stopped revolving).

The credit card may simply serve as a form of revolving credit, or it may become a complicated financial instrument with multiple balance segments each at a different interest rate, possibly with a single umbrella credit limit, or with separate credit limits applicable to the various balance segments. Usually this compartmentalization is the result of special incentive offers from the issuing bank, either to encourage balance transfers from cards of other issuers, or to encourage more spending on the part of the customer. In the event that several interest rates apply to various balance segments, payment allocation is generally at the discretion of the issuing bank, and payments will therefore usually be allocated towards the lowest rate balances until paid in full before any money is paid towards higher rate balances. Interest rates can vary considerably from card to card, and the interest rate on a particular card may jump dramatically if the card user is late with a payment on that card or any other credit instrument, or even if the issuing bank decides to raise its revenue. As the rates and terms vary, services have been set up allowing users to calculate savings available by switching cards, which can be considerable if there is a large outstanding balance (see external links for some on-line services).

Because of intense competition in the credit card industry, credit providers often offer incentives such as frequent flier points, gift certificates, or cash back (typically up to 1 percent based on total purchases) to try to attract customers to their program.

Low interest credit cards or even 0% interest credit cards are available. The only downside to consumers is that the period of low interest credit cards is limited to a fixed term, usually between 6 and 12 months after which a higher rate is charged. However, services are available which alert credit card holders when their low interest period is due to expire. Most such services charge a monthly or annual fee. credit card's grace period is the time the customer has to pay the balance before interest is charged to the balance. Grace periods vary, but usually range from 20 to 30 days depending on the type of credit card and the issuing bank. Some policies allow for reinstatement after certain conditions are met. Usually, if a customer is late paying the balance, finance charges will be calculated and the grace period does not apply. Finance charge(s) incurred depends on the grace period and balance, with most credit cards there is no grace period if there's any outstanding balance from the previous billing cycle or statement (ie. interest is applied on both the previous balance and new transactions). However, there are some credit cards that will only apply finance charge on the previous or old balance, excluding new transactions.

For merchants, a credit card transaction is often more secure than other forms of payment, such as checks, because the issuing bank commits to pay the merchant the moment the transaction is authorized, regardless of whether the consumer defaults on their credit card payment (except for legitimate disputes, which are discussed below, and can result in charge backs to the merchant). In most cases, cards are even more secure than cash, because they discourage theft by the merchant's employees.

For each purchase, the bank charges a commission (discount fee), to the merchant for this service and there may be a certain delay before the agreed payment is received by the merchant. The commission is often a percentage of the transaction amount, plus a fixed fee. In addition, a merchant may be penalized or have their ability to receive payment using that credit card restricted if there are too many cancellations or reversals of charges as a result of disputes. Some small merchants require credit purchases to have a minimum amount (usually between $5 and $10) to compensate for the transaction costs, though this is not always allowed by the credit card consortium.

In some countries, like the Nordic countries, banks guarantee payment on stolen cards only if an ID card is checked and the ID card number/civic registration number is written down on the receipt together with the signature. In these countries merchants therefore usually ask for ID. Non-Nordic citizens, who are unlikely to possess a Nordic ID card or driving license, will instead have to show their passport, and the passport number will be written down on the receipt, sometimes together with other information. Some shops use the card's PIN code for identification, and in that case showing an ID card is not necessary.

Authorization: When the cardholders pays for the purchase, the merchant performs some risk assessment and may submit the transaction to the acquirer for authorization. The acquirer verifies with the issuer—almost instantly—that the card number and transaction amount are both valid, and informs the merchant on how to proceed. The issuer may provisionally debit the funds from the cardholder's credit account at this stage.

Batching: After the transaction is authorized it is then stored in a batch, which the merchant sends to the acquiring bank later to receive payment (usually at the end of the day).

Clearing and settlement: The acquiring bank sends the transactions in the batch through the card association, which debits the card-issuing bank for the transaction amount, and credits the acquirer for the transaction amount minus the interchange fee.

Funding: The acquiring bank pays the merchant. The amount the merchant receives is equal to the transaction amount minus the discount rate charged by the acquiring bank to the merchant for the service.

The entire process, from authorization to funding, usually takes about 2-7 business days. However, many merchant card processors offer next-day deposits to customers subject to type of banking account.

In the event of a chargeback (when there's an error in processing the transaction or the cardholder disputes the transaction), the issuer returns the transaction to the acquirer for resolution. The acquirer then forwards the chargeback to the merchant, who must either accept the chargeback or contest it.

Commodity money is any money that is both used as a general purpose medium of exchange and as a tradable commodity in its own right.

Commodity based currencies are often viewed as more stable, but this is not always the case. The value of a commodity based currency as a medium of exchange depends on its supply relative to other goods and services available in the economy. Historically, gold, silver and other metals commonly used in commodity based monetary systems have been subject to regular and sometimes extraordinary fluctuations in purchasing power. This not only damages its stability as a medium of exchange; it also reduces its effectiveness as a store of value. In the 1500s and 1600s huge quantities of gold and even larger amounts of silver were discovered in the New World and brought back to Europe for conversion into coin. As a result, the purchasing power of those coins fell by 60% to 80%, i.e. the prices of goods rose, because the supply of goods did not keep pace with the increased supply of money. In addition, the relative value of silver to gold shifted dramatically downward. Such discoveries of huge sources of gold or silver are a thing of the past, and lend to their supply stability. More recently, from 1980 to 2001, gold was a particularly poor store of value, as gold prices dropped from a high of $850/oz. ($27.30 /g) to a low of $255/oz. ($8.20 /g).It should be noted that gold was not a currency at this time, and was fluctuating due to its status as a final store of value — that is, the price never goes to zero as fiat currencies inevitably do. The advantage of gold and silver, however, lies in the fact that, unlike fiat paper currency, the supply cannot be increased arbitrarily by a central bank.

It is also possible for the trading value of a commodity money to be greater than its value as a medium of exchange when governments attempt to fix exchange rates between different commodity monies. When this happens people will often start melting down coins and reselling the metal used to make them. This has happened periodically in the United States, eventually causing it to move away from pure silver nickels and pure copper pennies. Shipping coins from one jurisdiction to another so that they could be reminted was sometimes a lucrative trade before the advent of trusted paper money.

Commodity money's ability to function as a store of value is also limited by its very nature. Copper and tin risk rust and corrosion. Gold and silver are soft metals that can lose weight through scratches and abrasions, but this is nothing by comparison to fiat currencies, where billions of dollars can be injected ("printed") into the market within moments.

Stability aside, commodity-based currencies may have a tendency to restrain growth in a very active economy. For example, in order to maintain the price level, the supply of money in an any economy must be equal or greater than the volume of goods and services produced. If commodities are used as money, then the total production can easily outstrip the supply of those commodities, which leads to price deflation. The lower prices of goods would signal to their producers to reduce the supply of goods, hence restoring the price level. As such, production within commodity-based economies tends to be limited by the supply of the commodity currency.[citation needed]

This problem is compounded by the fact that money also serves as a store of value. This encourages hoarding (in other circumstances known as "saving")and takes the commodity money out circulation, reducing the supply. The supply of circulating commodity currency is further reduced by the fact that commodity moneys also have competing non-monetary uses. For example, gold and silver are used in jewelry, and nickel and copper have important industrial uses.

Commodity based currencies also limit the geographic extent of the trading market. To make large purchases either a large volume or a high weight or both of the commodity must be transported to the seller. The cost of transportation of the currency raises the transaction cost and makes long distance sales less attractive

If your credit card uses different rates for purchases, transfers, and cash advances, realize that the card issuer may pay the lower interest rate balance first. Consequently, if you carry a balance, your high-rate cash advance may not be "paid" until all lower-rate balances are paid in full.

Fixed-Rate credit cards are not fixed forever. Rates can be changed at any time, as long as the card issuer provides 15 days advance notice of the change in terms. Fees may also increase. These "Change in Terms" notices are usually included with your monthly statement.

Your interest rate may dramatically increase if you make late payments. For example, some issuers will raise your interest rate to the maximum after one or two late payments. Consequently, your 12% credit card could quickly turn into a 25% credit card.

Your credit card issuer may also raise your interest rate after conducting a routine credit report review. If your overall credit history has deteriorated, the issuer may raise your interest rate, even though you've never made a late payment on the card in question.

The 25 day grace period only applies when you pay-off your entire balance due each month. If you only pay the minimum payment, interest is immediately accrued from the moment you charge something to your credit card. Some companies are also shortening the grace period to 20 days, and some cards have no grace periods.

Ignore offers to reduce or skip payments. These options are frequently offered over the holidays. When you skip a payment, the loan continues to accrue interest; therefore, these offers simply increase the overall interest and finance charges that the creditor collects. On a similar note, beware of offers of no payment/no interest for a period of time. Furniture stores, jewelry stores, and electronics stores frequently offer these programs. For example, no payment/no interest for 12 months!! This can be a good offer, but once again, read the fine print. Make sure you know the details of the program. Generally, you need to pay off the entire balance before the end of the "free" period to receive the benefit. Otherwise, you will probably have to pay interest on the entire balance from the date of your purchase

Debt1consolidation.com entails taking out one loan to pay off many others. This is often done to secure a lower interest rate, secure a fixed interest rate or for the convenience of servicing only one loan.

Debt1consolidation.com can simply be from a number of unsecured loans into another unsecured loan, but more often it involves a secured loan against an asset that serves as collateral, most commonly a house. In this case, a mortgage is secured against the house. The collateralization of the loan allows a lower interest rate than without it, because by collateralizing, the asset owner agrees to allow the forced sale (foreclosure) of the asset to pay back the loan. The risk to the lender is reduced so the interest rate offered is lower.

Sometimes, debt consolidation companies can discount the amount of the loan. When the debtor is in danger of bankruptcy, the debt consolidator will buy the loan at a discount. A prudent debtor can shop around for consolidators who will pass along some of the savings. Consolidation can affect the ability of the debtor to discharge debts in bankruptcy, so the decision to consolidate must be weighed carefully.

Debt consolidation is often advisable in theory when someone is paying credit card debt. Credit cards can carry a much larger interest rate than even an unsecured loan from a bank. Debtors with property such as a home or car may get a lower rate through a secured loan using their property as collateral. Then the total interest and the total cash flow paid towards the debt is lower allowing the debt to be paid off sooner, incurring less interest. In practice, many people are in credit card debt because they spend more than their income. If that habit continues, the consolidation will not benefit them much because they will simply increase their credit card balances again.

Because of the theoretical advantage that debt consolidation offers a consumer that has high interest debt balances, companies can take advantage of that benefit of refinancing to charge very high fees in the debt consolidation loan. Sometimes these fees are near the state maximum for mortgage fees. In addition, some unscrupulous companies will knowingly wait until a client has backed themselves into a corner and must refinance in order to consolidate and pay off bills that they are behind on the payments. If the client does not refinance they may lose their house, so they are willing to pay any allowable fee to complete the debt consolidation. In some cases the situation is that the client does not have enough time to shop for another lender with lower fees and may not even be fully aware of them. This practice is known as predatory lending Certainly many, if not most, debt consolidation transactions do not involve predatory lending.

Credit card debt is an example of unsecured consumer debt, accessed through plastic credit cards.

Debt results when a client of a credit card company purchases an item or service through the card system. Debt accumulates and increases via interest and penalties when the consumer does not pay the company for the money he or she has spent.

The results of not paying this debt on time are that the company will charge a late payment penalty (generally in the US from $10 to $40) and report the late payment to credit rating agencies. Being late on a payment is sometimes referred to as being in "default". The late payment penalty itself increases the amount of debt the consumer has.

When a consumer has been late on a payment, it is possible that other creditors, even creditors the consumer was not late in paying, may increase the interest rates the consumer is paying. This practice is called universal default.

If the customer is carrying an amount of debt that is so high that it is over their credit limit, then they might be charged an over-the-limit fee of up to $39 until their balance is paid down to below their credit limit. This, too, may add to the consumer's debt.

Sometimes the late fees, over-the-limit fees, high annual percentage rates (APRs), and universal default overcome consumers who frequently do not pay off their debt, and the customer declares bankruptcy. If a customer files for bankruptcy, the credit card companies are required to forgive all or much of the debt, unless such discharge of debt is successfully challenged by one or more creditors, or blocked by a bankruptcy judge on legal grounds irrespective of creditors' challenges.

Because forgiveness of debt reduces likelihood of profit and continued survival, the companies are generally willing to offer another deal to the consumers in danger of bankruptcy. This deal consists of reduced APRs, removal of past late fees and penalty charges, and reaging the accounts so that the credit agencies see them as late accounts.A credit card is a system of payment named after the small plastic card issued to users of the system. A credit card is different from a debit card in that it does not remove money from the user's account after every transaction. In the case of credit cards, the issuer lends money to the consumer (or the user). It is also different from a charge card (though this name is sometimes used by the public to describe credit cards), which requires the balance to be paid in full each month. In contrast, a credit card allows the consumer to 'revolve' their balance, at the cost of having interest charged. Most credit cards are the same shape and size, as specified by the standard.

A user is issued credit after an account has been approved by the credit provider, and is given a credit card, with which the user will be able to make purchases from merchants accepting that credit card up to a pre-established credit limit. Often a general bank issues the credit, but sometimes a captive bank created to issue a particular brand of credit card, such as or Banks issues the credit.

When a purchase is made, the credit card user agrees to pay the card issuer. The cardholder indicates their consent to pay, by signing a receipt with a record of the card details and indicating the amount to be paid or by entering a Personal identification number (PIN). Also, many merchants now accept verbal authorizations via telephone and electronic authorization using the Internet, known as a Card not present (CNP) transaction.

Electronic verification systems allow merchants to verify that the card is valid and the credit card customer has sufficient credit to cover the purchase in a few seconds, allowing the verification to happen at time of purchase. The verification is performed using a credit card payment terminal or Point of Sale (POS) system with a communications link to the merchant's acquiring bank. Data from the card is obtained from a magnetic stripe or chip on the card; the latter system is in the United Kingdom commonly known as Chip an PIN, but is more technically an EMV card.

Other variations of verification systems are used by eCommerce merchants to determine if the user's account is valid and able to accept the charge. These will typically involve the cardholder providing additional information, such as the security code printed on the back of the card, or the address of the cardholder.

Each month, the credit card user is sent a statement indicating the purchases undertaken with the card, any outstanding fees, and the total amount owed. After receiving the statement, the cardholder may dispute any charges that he or she thinks are incorrect (see Fair Credit Billing Act for details of the US regulations). Otherwise, the cardholder must pay a defined minimum proportion of the bill by a due date, or may choose to pay a higher amount up to the entire amount owed. The credit provider charges interest on the amount owed (typically at a much higher rate than most other forms of debt). Some financial institutions can arrange for automatic payments to be deducted from the user's bank accounts.

Credit card issuers usually waive interest charges if the balance is paid in full each month, but typically will charge full interest on the entire outstanding balance from the date of each purchase if the total balance is not paid.

For example, if a user had a $1,000 outstanding balance and pays it in full, there would be no interest charged. If, however, even $1.00 of the total balance remained unpaid, interest would be charged on the $1 from the date of purchase until the payment is received. The precise manner in which interest is charged is usually detailed in a cardholder agreement which may be summarized on the back of the monthly statement. The general calculation formula most financial institutions use to determine the amount of interest to be charged is APR/100 x ADB/365 x number of days revolved. Take the Annual percentage rate (APR) and divide by 100 then multiply to the amount of the average daily balance divided by 365 and then take this total and multiply by the total number of days the amount revolved before payment was made on the account. Financial institutions refer to interest charged back to the original time of the transaction and up to the time a payment was made, if not in full, as RRFC or residual retail finance charge. Thus after an amount has revolved and a payment has been made that the user of the card will still receive interest charges on their statement after paying the next statement in full (in fact the statement may only have a charge for interest that collected up until the date the full balance was paid...i.e. when the balance stopped revolving).

The credit card may simply serve as a form of revolving credit, or it may become a complicated financial instrument with multiple balance segments each at a different interest rate, possibly with a single umbrella credit limit, or with separate credit limits applicable to the various balance segments. Usually this compartmentalization is the result of special incentive offers from the issuing bank, either to encourage balance transfers from cards of other issuers, or to encourage more spending on the part of the customer. In the event that several interest rates apply to various balance segments, payment allocation is generally at the discretion of the issuing bank, and payments will therefore usually be allocated towards the lowest rate balances until paid in full before any money is paid towards higher rate balances. Interest rates can vary considerably from card to card, and the interest rate on a particular card may jump dramatically if the card user is late with a payment on that card or any other credit instrument, or even if the issuing bank decides to raise its revenue. As the rates and terms vary, services have been set up allowing users to calculate savings available by switching cards, which can be considerable if there is a large outstanding balance (see external links for some on-line services).

Because of intense competition in the credit card industry, credit providers often offer incentives such as frequent flier points, gift certificates, or cash back (typically up to 1 percent based on total purchases) to try to attract customers to their program.